|

DSP Ultra Short Fund An open ended ultra-short term debt scheme investing in debt and money market securities such that the Macaulay duration of the portfolio is between 3 months and 6 months (please refer page no. 21 under the section “Where will the Scheme invest?” in the SID for details on Macaulay’s Duration) |

|

|

Enhanced cash fund

Suitable for investing surplus cash over short-term, alternative to on-demand deposits

Kedar Karnik

Total work experience of 13 years.

Managing this Scheme since

July 2016.

Rahul Vekaria

Total work experience of 7 years.

Managing this Scheme since

February 2018

Ultra Short Duration

Jul 31, 2006

CRISIL Ultra Short Term Debt Index

| Regular Plan | |

| Growth: | ₹ 2613.0287 |

| Direct Plan | |

| Growth: | ₹ 2738.2893 |

₹ 2,384 Cr

₹ 2,403 Cr

| Regular Plan : | 1.00% |

| Direct Plan : | 0.29% |

0.39 years

> 3 months

2,384

| Modified Duration | 0.37 years |

| Yield To Maturity | 5.19% |

Nil

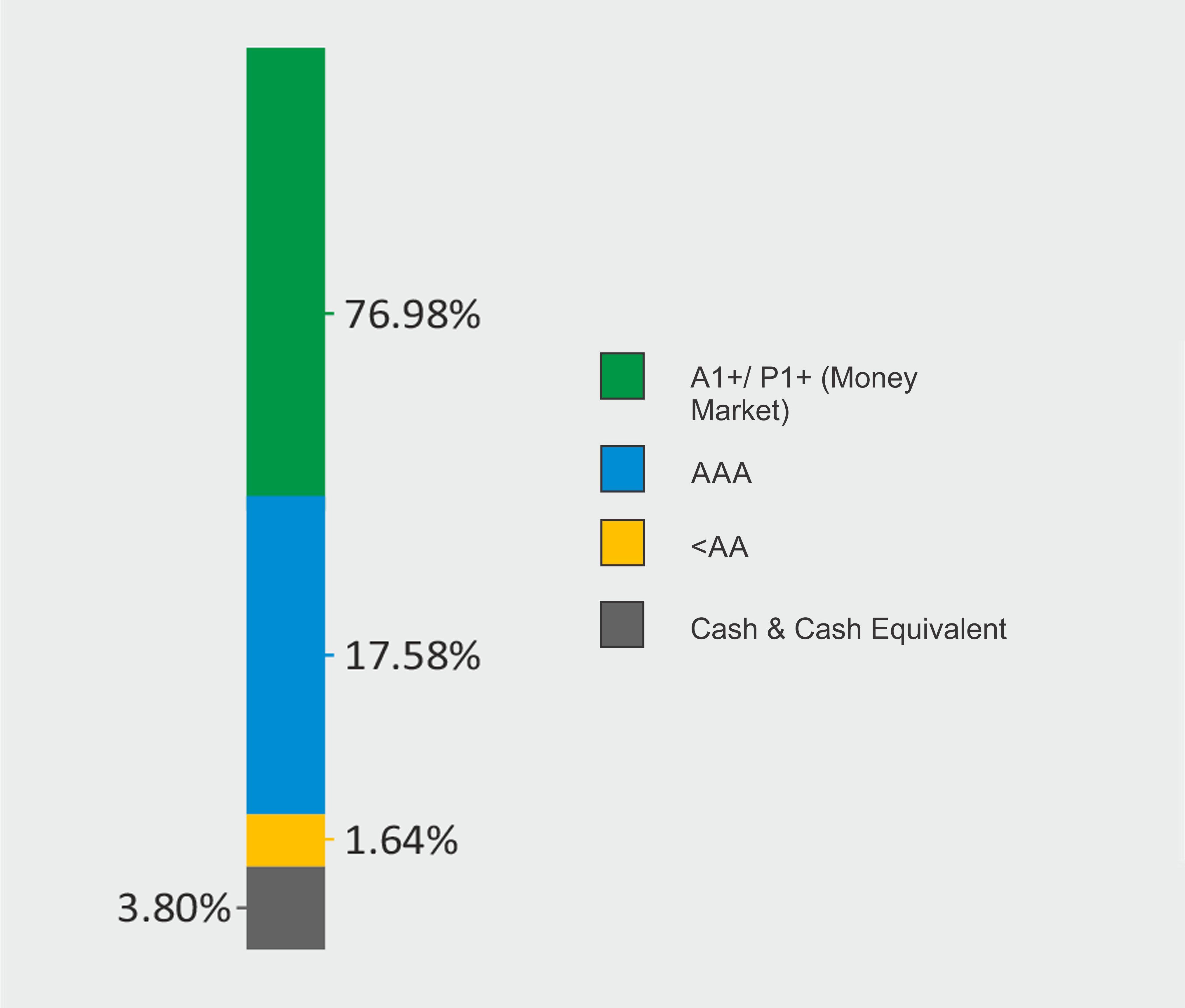

| Name of Instrument | Rating | % to Net Assets |

| DEBT INSTRUMENTS | ||

| BOND & NCD's | ||

| Listed / awaiting listing on the stock exchanges | ||

| ✔ Power Finance Corporation Limited | CRISIL AAA | 6.95% |

| REC Limited | CRISIL AAA | 3.57% |

| Housing Development Finance Corporation Limited | CRISIL AAA | 3.35% |

| Bajaj Finance Limited | CRISIL AAA | 2.17% |

| Muthoot Finance Limited | CRISIL AA | 1.64% |

| LIC Housing Finance Limited | CRISIL AAA | 1.11% |

| National Housing Bank | CARE AAA | 0.43% |

| Total | 19.22% | |

| MONEY MARKET INSTRUMENTS | ||

| Certificate of Deposit | ||

| ✔ ICICI Bank Limited | ICRA A1+ | 8.72% |

| ✔ Small Industries Development Bank of India | CARE A1+ | 8.11% |

| ✔ Bank of Baroda | IND A1+ | 6.15% |

| ✔ National Bank for Agriculture and Rural Development | IND A1+ | 5.34% |

| ✔ Axis Bank Limited | ICRA A1+ | 5.17% |

| ✔ Kotak Mahindra Bank Limited | CRISIL A1+ | 4.17% |

| Export-Import Bank of India | CRISIL A1+ | 4.07% |

| Axis Bank Limited | CRISIL A1+ | 2.08% |

| Indian Bank | IND A1+ | 2.08% |

| National Bank for Agriculture and Rural Development | CRISIL A1+ | 2.05% |

| Small Industries Development Bank of India | CRISIL A1+ | 1.00% |

| Total | 48.94% | |

| Commercial Paper | ||

| Listed / awaiting listing on the stock exchanges | ||

| ✔ Housing Development Finance Corporation Limited | CRISIL A1+ | 5.15% |

| ✔ Kotak Mahindra Prime Limited | CRISIL A1+ | 5.14% |

| ✔ Reliance Industries Limited | CRISIL A1+ | 4.12% |

| Export-Import Bank of India | CRISIL A1+ | 4.10% |

| Standard Chartered Investments and Loans (India) Limited | CRISIL A1+ | 3.92% |

| Chennai Petroleum Corporation Limited | CRISIL A1+ | 3.34% |

| Reliance Industries Limited | CARE A1+ | 2.27% |

| Total | 28.04% | |

| TREPS / Reverse Repo Investments / Corporate Debt Repo | 4.23% | |

| Total | 4.23% | |

| Cash & Cash Equivalent | ||

| Net Receivables/Payables | -0.43% | |

| Total | -0.43% | |

| GRAND TOTAL | 100.00% |

✔ Top Ten Holdings

DSP Ultra Short Fund erstwhile known as DSP Money Manger Fund

Notes: 1. All corporate ratings are assigned by rating agencies like CRISIL, CARE, ICRA, IND.

2. Pursuant to SEBI circular SEBI/HO/IMD/DF4/CIR/P/2019/102 dated September 24, 2019 read with

circular no. SEBI/HO/IMD/DF4/CIR/P/2019/41 dated March 22, 2019. Below are the details of the

securities in case of which issuer has defaulted beyond its maturity date.

| Security | ISIN |

value of the security

considered under net

receivables (i.e. value

recognized in NAV in

absolute terms and as

% to NAV) (Rs.in lakhs) |

total amount

(including

principal and

interest) that

is due to the

scheme on that

investment (Rs.in lakhs) | |

| 0% IL&FS Transportation Networks Limited Ncd Series A 23032019 | INE975G08140 | 0.00 | 0.00% | 6,627.81 |

| Performance (CAGR Returns in %) | ||||

| 1 m | 3 m | 6 m | 1 yr | |

| 6.95 | 5.49 | 5.36 | 6.68 | |

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments. Returns are for Regular Plan - Growth Option Click here for performance in SEBI prescribed format.

An Open ended income Scheme,

seeking to generate returns

commensurate with risk from a

portfolio constituted of money

market securities and/or debt

securities.

There is no assurance that the

investment objective of the

Scheme will be realized.

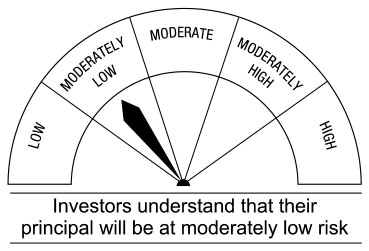

This Scheme is suitable for investors who are seeking*

• Income over a short-term investment horizon

• Investment in money market and debt securities

* Investors should consult their financial advisors if in doubt whether the product is suitable for them.